AI and the Reinvention of Commercial Banking Handoffs

30 January, 2026

Key Takeaways

- Escalations reveal the real CX failure. Banks lose customer primacy at system handoffs.

- Time tolerance has collapsed. FedNow and embedded finance reset expectations for instant resolution, not multi-day workflows.

- Orchestration is now a compliance issue. CFPB monitoring elevates fragmented escalation handling into regulatory risk.

- Fintech competes on memory. Unified data, microservices, and persistent context enable continuous journeys banks struggle to match.

- AI enables real-time coordination. LLMs assemble sentiment, transaction, and behavioral signals across fraud, ops, and compliance.

- Intent-to-resolution protects primacy. Application Assembly Layer (AAL) governs AI across existing systems, preserving context end-to-end without core replacement.

U.S. commercial banks are being hollowed out at the handoff. New payment infrastructure and AI-native competitors have shifted customer expectations faster than bank operating models have adapted, leaving banks no longer leading on innovation or experience.

FedNow eliminated customer patience for multi-day resolution. The Consumer Financial Protection Bureau (CFPB) eliminated plausible deniability for fragmented complaint handling. Fintech eliminated tolerance for starting over at every escalation.

In this ecosystem, customers do not announce they are leaving. They simply stop escalating to institutions that lose intent mid-journey and route critical transactions elsewhere.

Commercial banking has evolved significantly over the past decades with banks and alternate payment management applications reducing friction and improving consumer experience at each touchpoint. Multi-channel access, real-time responsiveness, and seamless digital journeys have rewired how customers expect to interact with financial institutions. This in large part has been accelerated by smart devices with mobile-first platforms now dominating customer engagement in commercial banking.

Real-time payment rails like FedNow settle transactions in seconds, collapsing tolerance for delayed responses (Federal Reserve, 2026).

The Infrastructure Dilemma

With the introduction of artificial intelligence (AI), financial service providers have enabled real-time personalization and context-aware service standards across digital commerce, exposing the gap when banks can't deliver it (McKinsey, 2024).

Traditional banks are paying the price for inaction. Their legacy systems were built to process transactions, not orchestrate intelligence, leaving them fundamentally unprepared for AI at scale. Neobanks and embedded finance providers win primacy by preserving customer intent across systems, not by adding channels (IBM, 2024).

The shift is categorical. Nonbank platforms now own the customer interface, while banks increasingly supply regulated infrastructure behind the scenes (PwC, 2024).

Artificial intelligence is amplifying these expectation gaps. Proactive intervention is now the baseline, and repetition during escalation has become intolerable in customer experience (CX).

Moreover, regulatory pressure is intensifying. In 2024, the CFPB recorded nearly 2.8 million consumer complaints, elevating fragmented escalation handling into a clear regulatory risk amid expanded oversight (CFPB, 2024).

Traditional banks now face dual pressure: prove they can detect friction across fragmented systems, while competing against AI-native players that eliminate friction by design.

U.S. businesses lose $1.4 trillion annually due to CX failures (The Financial Brand, 2025).

For commercial banks, this failure concentrates at the handoff, where fragmented systems break continuity and erode primacy.

Trust no longer belongs to banks by default. It relocates to whoever preserves intent while keeping the customer experience friction-less.

Learn More: Disruption at the Door - AI and the Re-Architecture of Commercial Banking

When Channel Excellence is Not Enough

Banks optimized for isolated touchpoint performance in an era where customers now expect fintech-grade orchestration across fragmented systems.

The first response to digital disruption was channel expansion. Mobile apps, online portals, chatbots, and call centers now provide multiple access points, yet customer experience infrastructure was never architected to preserve context across them. As channel proliferation accelerated, coordination between systems remained sequential.

Most banks still operate fragmented CX stacks: separate platforms for CRM, contact centers, fraud detection, online banking, branch operations, and compliance documentation. Each system is optimized for a single channel or function, with automation applied in isolation. Customer data is captured, but contextual continuity is lost at every handoff.

AI-driven sentiment analysis may detect frustration in a chat interaction, but it cannot connect that signal to a fraud investigation happening simultaneously in operations or a compliance review triggered three days earlier. These tools were never designed to maintain persistent customer intent across departments, a gap that becomes urgent as fintech competitors architect systems where context loss is structurally impossible.

Legacy banks operate on sequential, case-driven workflows; architectures designed for orderly handoffs rather than real-time orchestration across parallel systems. Modern CX now requires simultaneous visibility into transaction history, communication threads, operational status, and fraud signals. That’s a level of interoperability that channel-specific systems cannot deliver at the pace customers expect.

At the same time, pressure to act is mounting. While 51% of banks recognize that AI is fundamentally reshaping customer expectations, only 26% report meaningful improvements in cross-channel experience delivery today (KPMG, 2025). Governance gaps, fragmented data, and siloed ownership have kept CX modernization tactical rather than architectural.

Banks now face an architectural gap where orchestration is expected. But without an execution layer that governs intelligence across systems, fintech-grade continuity remains structurally unattainable.

Learn More: How Web 3.0 and Blockchain are Transforming FinTech?

How Fintech Built Memory into the Architecture

While banks debated channel integration strategies and governance frameworks, fintech rebuilt the customer experience stack for persistent context and zero-handoff resolution.

Context Persistence as Foundational Requirement

Fintech platforms built on instant settlement and limited recourse couldn't tolerate context loss. Persistence became foundational infrastructure from launch, rather than a feature added later.

Neobanks and embedded finance providers architected systems where customer intent persists across sessions, channels, and transactions without degradation. Support flows tie directly to transaction state. When a customer initiates a dispute on mobile, continues via chat, and escalates through email, the platform maintains a single narrative thread without repetition, information loss, or departmental handoffs that reset urgency.

Unified Data Architecture Enabled Speed

Fintech consolidated capabilities that traditional banks historically deployed in isolation. Customer data platforms centralize touchpoint data across web, mobile, support, and transaction systems in real time. Profile updates flow to all channels simultaneously.

Revolut exemplifies this approach. Secure API connections link external bank accounts to provide unified spending insights, budgeting features, and seamless fund transfers without requiring customers to reconcile data manually (Revolut, 2024).

This real-time data processing capability enables fintech platforms to deliver personalized financial advice, fraud detection, and predictive analytics at scale.

Microservices Architecture Accelerated Iteration

API-first, modular infrastructure allowed fintech to swap vendors, integrate authentication methods, and test models without rewriting core systems.

Microservices architecture breaks monolithic platforms into smaller, independent services that can be developed, deployed, and scaled separately. This allows new features to roll out faster without adding extra technical debt.

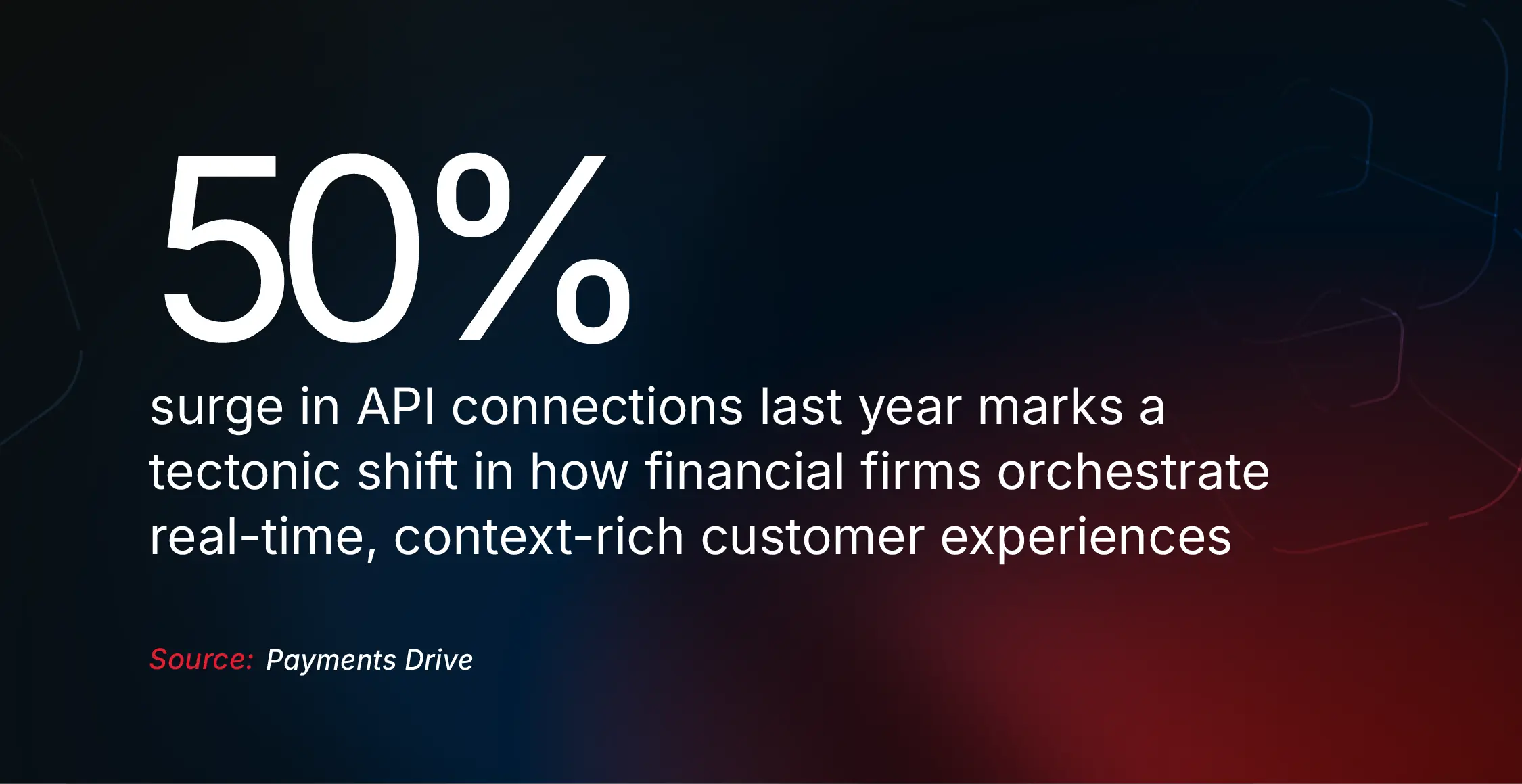

API connections between financial companies grew 50% in the past year, reaching around 114 million (Payments Dive, 2025). The surge reflects how open banking regulations, such as CFPB Section 1033, transformed API access from an optional feature to market infrastructure (CFPB, 2025).

Fintech platforms architected for unified API access gained immediate advantage: instant account verification, cross-border remittances with full transaction context, and real-time account aggregation became operationally viable at scale.

The Compounding Competitive Divide

The gap between banks and fintech is widening. Fintech platforms built orchestration into their architecture from day one. Banks, by contrast, layer integration on top of existing systems, creating friction and complexity. Each new digital channel or feature adds fragmentation and overhead, while every fintech innovation reinforces an infrastructure that accelerates speed, context continuity, and risk-managed experimentation.

This structural advantage sets the stage for the context-native era, where customer expectations demand memory, speed, and continuity across every touchpoint.

What the Context-Native Era Demands

Customer experience orchestration is no longer confined to channel optimization or interface design. It now determines whether banks can detect, interpret, and resolve friction before customers stop escalating to them entirely.

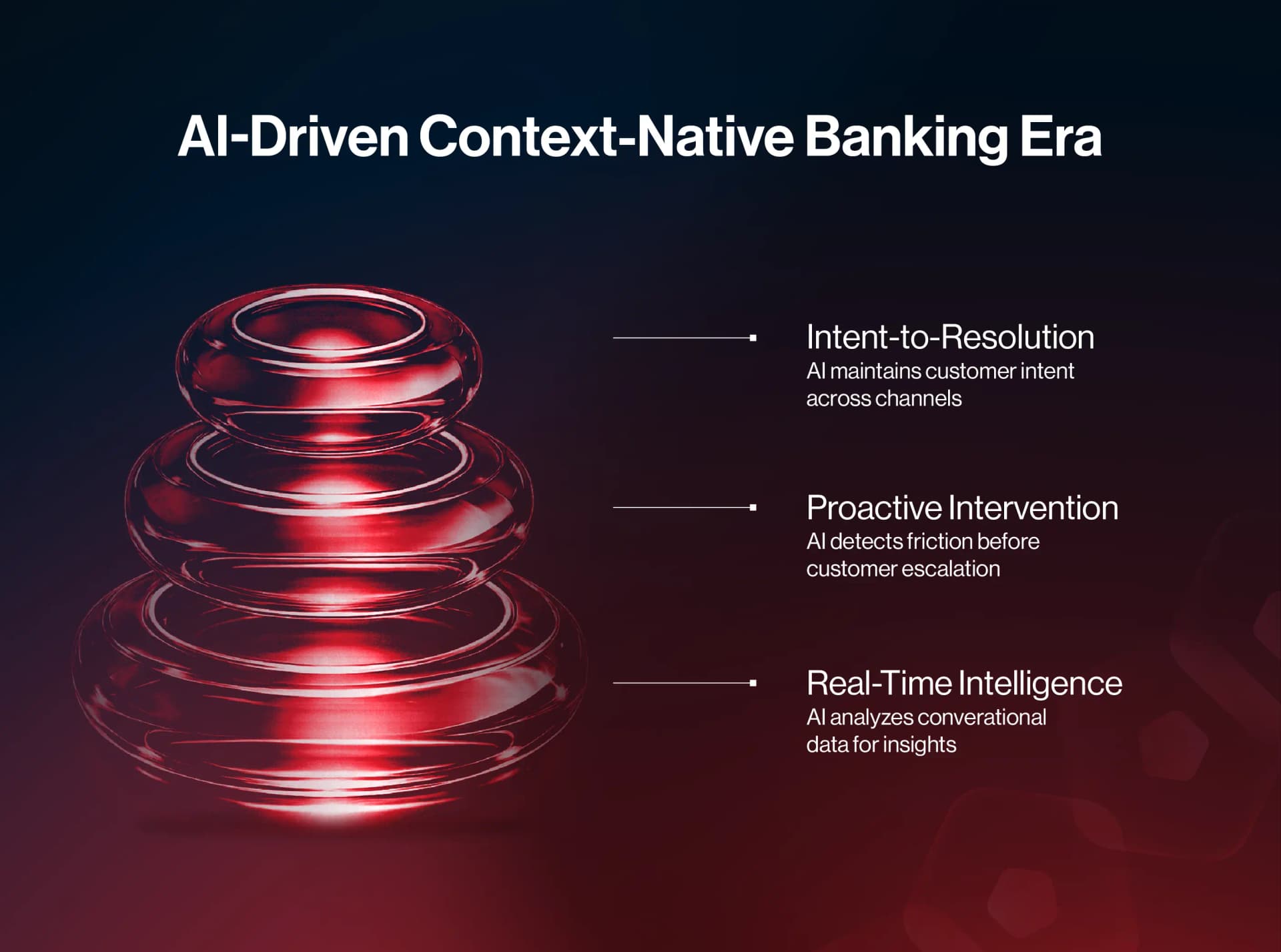

Real-Time Intelligence at Scale

Large language models enable real-time analysis of conversational data across channels in ways that were technically impossible even two years ago. These systems detect sentiment degradation within interactions, identify emerging pain point patterns before they crystallize into formal complaints, and flag churn risk signals that traditional rule-based systems miss.

When a commercial client’s wire transfer stalls and they contact support twice within 24 hours using different channels, AI can detect the escalating urgency and route the issue to coordinated resolution.

From Reactive to Proactive Intervention

Previous-generation analytics identified problems after resolution failed. AI-driven orchestration surfaces friction while journeys are still in progress, creating intervention opportunities before customer trust erodes.

This allows banks to operationalize regulatory demands and customer expectations by detecting dissatisfaction proactively and resolving it with context intact from first signal to final outcome.

Intent-to-Resolution Orchestration as a New Standard

The context-native era demands intent-to-resolution orchestration. Customer intent must persist as a single, continuous thread across all departments, channels, and systems, coordinated through a governance layer that enforces policy, preserves auditability, and enables intervention at every handoff.

Platforms architected for persistent context are setting new expectations for memory and trust. Banks must meet them without sacrificing the regulatory control that differentiates them.

Learn More: Redefining Industrial Resilience: How AI Infrastructure Delivers Adaptive Advantage

Can Banks Preserve Context Without Destabilizing Core Systems?

The demands are clear. The question is whether traditional banks can meet them without destabilizing the core systems that regulators, auditors, and operations depend on.

The answer lies not in replacement, but in reimagining how intelligence flows across legacy infrastructure.

Moreover, banks hold structural advantages that fintech platforms don't:

- Institutional trust built over decades

- Regulatory relationships that enable complex product offerings

- Comprehensive customer financial graphs spanning deposits, lending, treasury services, and investment relationships.

The challenge lies in translating these assets into coordinated, real-time customer experience delivery without sacrificing the governance that makes them possible.

A North American retail bank faced legacy hurdles while delivering personalized offers. By deploying an AI-driven orchestration platform, it tripled personalization, cut approval times by 75%, lowered costs, and ensured compliance, all without disrupting customer journeys (Capgemini, 2026). This shows how AI and orchestration turn systemic friction into measurable CX advantage.

The path forward requires an orchestration layer that governs intelligence across existing systems, transforming architectural liability into a competitive advantage without forcing banks to choose between speed and control.

Orchestrating Context Across Systems

In order to preserve the value chain for most banking and financial institutions, one solution is to develop a new application layer that functions as the governance interface between legacy infrastructure and AI-driven workflows. This layer is something we define as the Application Assembly Layer (AAL), a layer that allows AI models and Agentic Solutions to interface with legacy infrastructure and systems such as CRM platforms, call-center infrastructure, branch applications, and compliance tools, etc., enabling them to orchestrate real-time context flow without replacing underlying systems.

AAL enforces policy constraints, maintains audit trails, ensures regulatory compliance, and enables sub-second context transfer across channels.

Integration platforms connect systems; orchestration platforms govern intelligence across systems. AAL provides both a unified data fabric combined with policy-constrained AI workflows that preserve context from first signal to final resolution.

When a commercial client escalates an issue through any channel, AAL maintains a single thread of intent across all subsequent interactions. Eliminating repetition, accelerating resolution, and generating compliance artifacts as execution unfolds.

This is how banks defend primacy, by owning the orchestration layer that makes continuous context operationally viable within regulatory boundaries.

The Path Forward: Pilot-First Orchestration

Commercial banking infrastructure evolved over decades to meet regulatory and operational demands. Replacing it isn't viable financially, operationally, or from a risk perspective. The alternative is assembling intelligence across existing systems with architectural discipline.

CodeNinja's approach utilizes proprietary tooling platforms like Hyper to build an Application Assembly Layer that orchestrates intelligence independently across CRM platforms, transaction systems, compliance workflows, and customer-facing channels. This enables banks to pilot intent-to-resolution orchestration without destabilizing core systems. The highest-urgency pilot focuses on cross-channel context continuity for high-value escalations, where context loss directly causes customer defection and compliance exposure.

Measurable outcomes include application completion rate improvement, ‘restart incident’ reduction, and accelerated mean time to resolution. Pilot duration is 60 to 90 days, with results visible within 30 days as orchestrated workflows begin handling live escalations.

U.S. commercial banking is not being disrupted at the front door. It's being hollowed out in the middle.

Every escalation where context dies trains customers to trust someone else with their next critical transaction. FedNow removed patience for multi-day resolution. CFPB removed plausible deniability for fragmented complaint handling. Fintech removed tolerance for repetition.

The banks that win will be the ones that never lose intent, especially when it matters most. Because in this ecosystem, customers don't announce they're leaving. They simply stop escalating to the bank and start routing their most important interactions elsewhere.

Launch a 60–90 day pilot to orchestrate customer context across channels, eliminate ‘start over’ moments, and prove measurable CX improvement, without disrupting core banking operations. Learn More

Bibliography

- Capgemini Research Institute. Capgemini Financial Services Top Trends 2026: Banking. January 2026. https://www.capgemini.com/wp-content/uploads/2025/12/Capgemini_Top-Trends-2026_Banking-1.pdf.

- Consumer Financial Protection Bureau. "Consumer Response Annual Report: January 1 - December 31, 2024." May 2025. https://files.consumerfinance.gov/f/documents/cfpb_cr-annual-report_2025-05.pdf

- Consumer Financial Protection Bureau. "Required Rulemaking on Personal Financial Data Rights." Accessed January 27, 2026. https://www.consumerfinance.gov/personal-financial-data-rights/.

- Federal Reserve. "FedNow Service: Additional Questions and Answers." Last updated December 3, 2024. https://www.federalreserve.gov/paymentsystems/fednow-additional-questions-and-answers.htm.

- The Financial Brand. “The Illusion of Good CX.” May 6, 2025. https://thefinancialbrand.com/news/customer-experience-banking/five-critical-gaps-in-banks-customer-experience-delivery-and-how-to-fix-them-188787

- IBM Institute for Business Value. " Embedded Finance: Creating the Everywhere, Everyday Bank." September 1, 2023. https://www.ibm.com/thought-leadership/institute-business-value/en-us/report/embedded-finance.

- KPMG International. Intelligent Banking: A Blueprint for Creating Value Through AI-Driven Transformation. February 2025. https://assets.kpmg.com/content/dam/kpmgsites/pl/pdf/2025/08/pl-Intelligent-banking-Report.pdf.coredownload.inline.pdf.

- McKinsey & Company. "Extracting Value from AI in Banking: Rewiring the Enterprise." December 9, 2024. https://www.mckinsey.com/industries/financial-services/our-insights/extracting-value-from-ai-in-banking-rewiring-the-enterprise.

- Payments Dive. "Open Banking Lurches Onward." November 3, 2025. https://www.paymentsdive.com/news/open-banking-lurches-onward/804397/.

- PwC. "Tech Translated: Embedded Finance." Last updated June 18, 2024. https://www.pwc.com/gx/en/issues/technology/tech-translated-embedded-finance.html.

- Revolut Developer Portal. "Developer Guides: Accounts and Transactions Syncing." Accessed January 27, 2026. https://developer.revolut.com/docs/guides/manage-accounts/use-cases/accounts-and-transactions-syncing.