The Binary Choice for US Banking: Orchestration Platform or Invisible Infrastructure

3 February, 2026

Executive Summary

Over the past decade, commercial banking has dispersed execution across digital channels and outsourced innovation to FinTech partnerships, but strategic control has remained concentrated in legacy architectures designed for a pre-digital era. The bottleneck has never been capital or technology access; it has been the inability to internalize, scale, and retain orchestration intelligence without accumulating architectural debt that compounds with every partnership, every pilot program, and every “digital transformation” initiative.

Historically, banking disruption was framed as the outcome of better products, lower fees, slicker apps, and faster approvals. Today, disruption is increasingly defined by who controls the orchestration layer that assembles those products into coherent customer experiences. As artificial intelligence becomes a foundational layer of financial services delivery, banks face a critical tension: how to accelerate capability without eroding strategic control. In many cases, speed has been prioritized over sovereignty, trading immediate revenue partnerships for long-term architectural subordination.

The question is no longer whether banks should adopt AI; it is whether banks will architect AI as the foundation of their orchestration capability or rent it as a utility while competitors own the customer relationship. This is not about technology adoption rates. It is about who builds the trust infrastructure that customers rely on when AI agents begin making financial decisions on their behalf.

The Real Crisis, Architectural Control, Not Technology Adoption

The Misdiagnosis

A closer examination of banking operations reveals why excellence often stalls despite record technology investments: banks have spent the past decade implementing AI as point solutions, fraud detection here, chatbot there, recommendation engine somewhere else, without building the underlying orchestration architecture that would allow these capabilities to function as an integrated intelligence system.

Consider the typical large bank’s current state. Despite significant AI investments and vendor partnerships, most institutions report limited value capture. The problem is not the technology itself but how it is deployed. Each AI initiative delivers localized benefits, faster fraud detection in one channel, better credit models for one product line, but these capabilities remain isolated. There is no fabric connecting them, no memory preserving their outputs, and no orchestration layer coordinating their collective intelligence.

The market recognizes this capability gap. Despite strong revenues, banking trades at significant valuation discounts compared to other industries (McKinsey Global Banking Annual Review, 2024). This penalty does not reflect current profitability; it reflects investor skepticism about banks’ ability to compete in an AI-native landscape where orchestration control determines market position.

The Data Gravity Inversion: How Banks Lost the Information Advantage

Banks historically owned customer relationships because they held transaction data. Every deposit, withdrawal, payment, and transfer created information that only banks could see. This data monopoly created structural power; banks knew their customers’ financial lives completely while customers knew only their own fragmented experiences.

But data gravity has inverted over the past decade, and most bank executives have not fully internalized the implications.

What Banks Know (Transaction Data):

- Post-execution transaction logs: what customers spent and where

- Stated preferences from applications and surveys, the lowest-fidelity data source

- Siloed product history that does not connect across divisions (mortgage teams unaware of credit card behavior, wealth advisors do not see checking patterns)

- Backward-looking analytics: what happened last month, last quarter, last year

What FinTechs and Digital Wallets Know (Behavioral Data):

- Pre-transaction intent: browsing history, shopping cart activity, price comparison behavior, merchant research

- Life event signals: job changes detected through income shifts, relocations visible in spending geography changes, major purchases indicating life transitions (new baby, home purchase, education)

- Inferred preferences: risk tolerance derived from actual financial decisions rather than survey responses; spending priorities visible through category allocation; brand affinities demonstrated through merchant loyalty

- Social and network context: peer spending patterns, influence networks, recommendation uptake, group behaviors

- Forward-looking predictions: what a customer will likely need next week, next month, or next year

The Information Advantage Reversal

Illustration 1: The Data Gravity Inversion - Banks once held information monopoly seeing complete customer financial lives. Today, digital wallets and FinTechs capture behavioral intelligence predicting future needs, while banks see only settled transactions stripped of context. This inversion fundamentally shifts who owns the customer relationship.

The outcome is stark. FinTechs understand customer intent before banks see transactions. By the time banks have data, decisions have already been made. Banks analyze history; competitors predict futures.

This inversion accelerates as payment flows migrate to digital wallets and AI agents. When a customer uses Apple Pay, Google Wallet, or embedded FinTech payment rails, the bank sees only the settled transaction, a data point stripped of context. The wallet provider sees the complete journey: what the customer browsed, compared, abandoned, reconsidered, and finally purchased. The wallet knows why; the bank knows only what.

The Partnership Trap: How Good Intentions Create Strategic Subordination

Faced with the FinTech innovation wave, most banks pursued what seemed a pragmatic strategy: partnership. Rather than competing directly with nimble startups unburdened by legacy systems and regulatory constraints, banks would provide what they possessed, capital, regulatory licenses, compliance infrastructure, and balance sheet capacity, while FinTechs would provide what banks struggled to build: modern interfaces, rapid innovation, and customer acquisition.

This approach appeared rational in board presentations. Revenue sharing agreements promised incremental income. Customer acquisition metrics showed growth. Innovation labs demonstrated technology adoption. But beneath these surface successes, structural control was eroding.

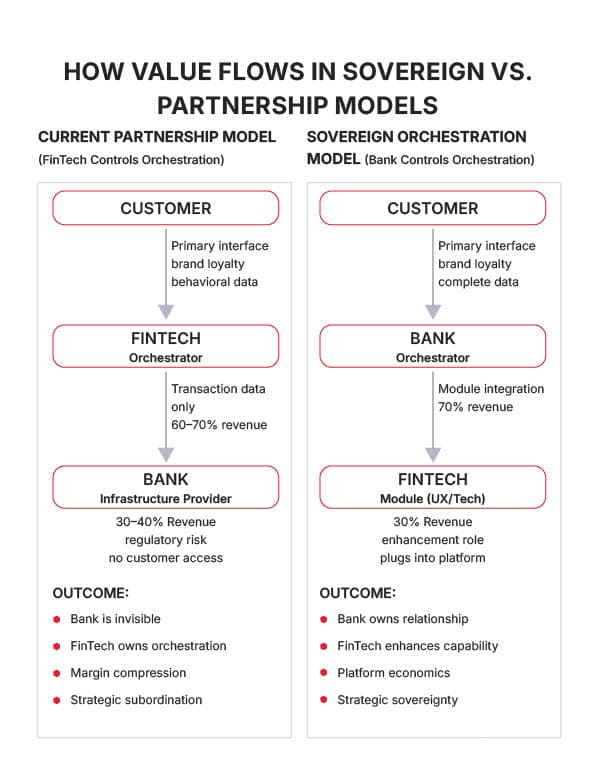

How Value Flows in Sovereign Vs. Partnership Models

Illustration 2: Partnership Value Flow - In current models, FinTechs capture 60-70% of revenue and 100% of behavioral data while banks bear regulatory risk for 30-40% returns. Sovereign orchestration inverts this dynamic, positioning banks as platforms and FinTechs as enhancement modules.

The Trust Infrastructure Problem: Who Do Customers Trust When AI Agents Transact?

As AI moves from assistance to agency, from tools that help humans make decisions to agents that make decisions autonomously, a new question emerges: where does trust reside?

Consider the near-future scenario already emerging in early deployments. A customer’s AI agent monitors their cash flow, identifies an upcoming shortfall, evaluates available credit options, negotiates terms with multiple lenders, and executes a loan transaction, all without human involvement beyond initial authorization. This is not science fiction; it is the logical extension of current AI capabilities applied to financial services.

In this scenario, critical questions arise:

Who validates the AI agent’s identity?

- If an agent claims to represent a customer, how is that claim verified? Current authentication models assume human interaction through passwords, biometrics, and device recognition. Agent-to-agent transactions require new trust infrastructure.

Who ensures the agent is acting in the customer’s interest?

- When AI negotiates financial terms, who verifies it is optimizing for the customer rather than hidden incentives embedded in its training data or commercial arrangements?

Who provides recourse when agents make mistakes?

- If an AI agent commits the customer to unfavorable terms, executes an unintended transaction, or misinterprets instructions, who bears responsibility? The customer who authorized the agent? The platform that deployed the agent? The bank that executed the transaction?

Who maintains the audit trail?

- When thousands of micro-transactions occur without human review, regulatory compliance requires comprehensive logging of agent decision-making, not just transaction records.

These questions reveal a critical gap in current banking architecture. There is no trust layer designed for AI-native transactions. Banks built trust infrastructure for human customers interacting through defined channels, and that infrastructure is inadequate for the emerging reality of AI agents oper

The entity that builds this trust layer, the infrastructure that authenticates agents, validates their authority, ensures aligned incentives, provides recourse mechanisms, and maintains compliance audit trails, will control the orchestration layer for AI-native financial services.

Currently, this infrastructure is being built by BigTech platforms and FinTech innovators, not traditional banks. Apple, Google, PayPal, and emerging AI-first FinTechs are establishing the standards, protocols, and architectures that will govern agent-to-agent financial transactions. Banks are participants in these ecosystems, not architects of them.

This represents a fundamental shift in banking’s structural position. For two centuries, banks were the trusted intermediaries in financial transactions. Trust flowed through banking relationships. Now, trust is migrating to orchestration platforms, and banks risk becoming invisible execution layers beneath interfaces they do not control and trust infrastructure they did not build.

Part II: The Orchestration Layer, Where Value Actually Resides

The Pattern Across Industries: Orchestration Beats Execution

The pattern of orchestration control determining industry structure is not unique to banking. It is observable across every technology-disrupted sector over the past two decades. Understanding these patterns provides insight into banking’s current trajectory and the structural forces at play.

Retail: Amazon’s Orchestration Dominance

Amazon does not manufacture most products it sells. It does not own the inventory sitting in third-party warehouses. It does not employ most of the people who pack and ship orders. Yet Amazon controls retail because it controls orchestration: the discovery layer through search and recommendations, the transaction layer through one-click purchasing, the fulfillment logic that determines which warehouse ships which item, and the customer relationship through Amazon Prime, not individual brands, which owns loyalty.

Retail brands became suppliers feeding Amazon’s orchestration engine. Customers identify with Amazon, not the underlying brands. When a customer buys a product “on

Amazon,” they often do not remember or care who manufactured it. The orchestrator owns the relationship; the executor becomes invisible.

Transportation: Uber’s Dispatch Control

Uber does not own vehicles. It does not employ drivers as traditional employees. It does not maintain infrastructure or garage fleets. Yet Uber controls urban transportation in hundreds of cities because it controls orchestration: the dispatch algorithm that matches riders to drivers, the pricing engine that manages surge pricing and route optimization, and the reputation system where ratings determine driver access to the platform.

Taxi operators and individual drivers became commodity labor feeding Uber’s orchestration platform. Customers do not request “a driver”; they request “an Uber.” The orchestrator owns the category; the executor becomes interchangeable.

Media: Netflix’s Recommendation Engine

Netflix started by licensing content it did not own. Today, even with significant original production, most of its catalog comes from external studios. Yet Netflix controls streaming entertainment because it controls orchestration: the recommendation algorithm that determines what to watch next, the bundling logic that governs how content is packaged and presented, and the viewing experience across interfaces, features, and devices.

Content producers became suppliers feeding Netflix’s content engine. Customers subscribe to Netflix, not to individual shows or studios. The orchestrator owns the audience; the creator becomes a content provider.

The Consistent Pattern

In every case, the entity controlling orchestration captured dominant value despite not controlling execution:

- They do not own the underlying assets, whether products, vehicles, content, or in banking’s case, capital and regulatory licenses

- They control the customer interface and decision logic, including how options are presented, what is recommended, and how transactions execute

- They capture behavioral data, including what customers browse, consider, abandon, and ultimately choose

- They own the customer relationship through brand identification, loyalty programs, and the primary touchpoint

The executors, the entities actually manufacturing products, driving cars, or creating content, become interchangeable suppliers competing on price and quality while lacking direct customer relationships.

Banking’s Orchestration Battle: The Current State

Banking is experiencing the same dynamic, but the outcome remains contested. The orchestration layer in financial services is currently being fought over by three categories of players:

Traditional Banks

Own execution infrastructure, including capital, regulatory licenses, compliance, and settlement, but increasingly lack control of customer interfaces and decision logic.

FinTechs and Neobanks

Control customer interfaces and decision logic but lack execution infrastructure, relying on partner banks for actual banking services.

BigTech Platforms

Control broader ecosystems such as devices, operating systems, and merchant relationships, and are inserting financial orchestration as a natural extension of existing customer relationships.

The strategic question is not who has better technology. All three categories can access similar AI capabilities. The question is who will control the orchestration layer where those technologies are deployed.

The Digital Wallet as Orchestration Beachhead

Digital wallets represent the most visible battleground for orchestration control. What began as payment convenience has evolved into the strategic high ground for customer relationship ownership.

First-Generation Wallets: Payment Convenience

Early digital wallets, including Apple Pay, Google Pay, and Samsung Pay, offered a simple value proposition: replacing physical cards with phone-based payments. Banks saw these as channels, convenient ways for customers to access bank-issued cards. The infrastructure remained bank-controlled; wallets functioned primarily as interfaces.

Second-Generation Wallets: Financial Orchestration Hubs

Current-generation wallets have evolved beyond payment convenience into financial orchestration platforms:

- Cash App is not just payments; it includes checking, investing, Bitcoin trading, tax filing, direct deposit, and lending

- Venmo is not just P2P transfers; it includes social payments, crypto, credit, merchant transactions, and brand partnerships.

- PayPal is not just checkout; it includes working capital loans, buy-now-pay-later, crypto custody, and savings accounts.

- Apple Wallet is not just Apple Pay; it now includes Apple Card, Apple Savings, and eventual expansion into investing and lending.

These platforms control the orchestration logic that was historically banking’s core function: when customers should save versus spend, when they need credit, how they should invest, and what insurance they need.

The wallet sees the customer’s complete financial life, including income through direct deposit, spending across transactions, saving through balance growth, investing via portfolio activity, and credit through loan usage. It knows life events before banks do because it observes behavioral signals in real time.

Third-Generation Wallets: AI Agent Platforms

The emerging generation embeds AI agents that act on the customer’s behalf:

- Automated savings agents that move money based on spending patterns

- Bill negotiation agents that identify overcharges and negotiate refunds

- Investment agents that rebalance portfolios based on goals and market conditions

- Credit optimization agents that refinance debt when better terms emerge

- Merchant loyalty agents that maximize rewards across fragmented programs

When these agents operate within wallet ecosystems, the wallet platform becomes the trust infrastructure customers rely on. Banks execute transactions initiated by the agents, but they do not control the agent logic, do not see the decision-making process, and do not own the customer relationship.

This is the partnership trap rendered algorithmic. Banks provide execution while platforms provide intelligence.

The Cross-Border Implications: When Orchestration Crosses Jurisdictions

The orchestration challenge intensifies in cross-border scenarios where traditional banking infrastructure is expensive, slow, and opaque, while digital-native orchestration platforms deliver superior experiences.

Traditional Cross-Border Banking:

- Multiple intermediary banks, each extracting fees

- Unclear foreign exchange rates with hidden spreads

- Settlement times measured in days

- Limited transparency into transaction status

- High friction for consumers and small businesses

Digital Orchestration Platforms (Wise, Revolut, Emerging Crypto Rails):

- Direct connections that minimize intermediaries

- Transparent FX rates published in real time

- Settlement in hours or minutes

- Complete transaction visibility

- Consumer-friendly interfaces and pricing

The customer experience gap is so pronounced that entire demographics, including immigrants sending remittances, freelancers receiving international payments, and travelers managing multi-currency spending, now default to digital platforms rather than traditional banks.

Banks still execute the underlying transactions. Someone must hold regulatory licenses in each jurisdiction, maintain nostro accounts, and settle with central banks. But banks are invisible infrastructure. The platform owns the relationship, controls pricing, determines the experience, and captures behavioral data about international financial flows.

As AI agents begin optimizing cross-border transactions by automatically routing through the cheapest corridors, timing FX conversions based on rate predictions, and splitting large transfers to minimize fees, the value of the orchestration layer increases while the value of the execution layer declines. Banks become commodity pipes; platforms become intelligent orchestrators.

Part III: The Sovereign Decision Fabric, Architecture for Independence

To reclaim orchestration control, banks require a fundamentally different architectural approach than the point solutions and vendor partnerships that have dominated the past decade. The Sovereign Decision Fabric represents this shift, not a product to purchase, but an architectural pattern to build, where AI systems, institutional knowledge, and operational workflows unite as coherent capability.

The SDF is not about having better AI models than competitors. It is about embedding AI as the orchestration infrastructure itself, the layer that preserves context, maintains decision authority, and ensures that intelligence compounds rather than fragments across vendor relationships and system silos.

The Three-Tier Architecture

Tier 1: Execution Intelligence Layer, From Reaction to Pre-Execution Governance

Traditional banking operates fundamentally reactively. Transactions execute, funds move, analysis happens later, whether minutes, hours, or days. Alerts generate and humans investigate. This creates a responsibility gap where losses accumulate before governance applies.

The Execution Intelligence Layer inverts this paradigm by applying intelligence before authorization rather than after execution:

Customer Request → Multi-Agent Intelligence Evaluation → Consensus Decision → Only If Approved, Execute

This shift means fraud is blocked before funds move, not detected after. Credit decisions incorporate real-time data, not stale snapshots. Risk assessment occurs before commitment, not during post-mortem review.

The technical foundation uses domain-specific AI models trained exclusively on banking data, including fraud detection patterns, credit performance outcomes, compliance monitoring, and customer intent signals. These models are deployed on bank-owned infrastructure rather than rented from cloud providers. They achieve superior performance in their specific domains while maintaining data sovereignty, a critical requirement as regulatory frameworks increasingly mandate that customer financial data remain under direct institutional control.

The real innovation, however, is architectural. Intelligence is embedded in the transaction flow itself, not bolted onto existing systems. Every authorization passes through evaluation. Every decision preserves its rationale. Every outcome feeds back to improve future decisions.

Tier 2: Orchestration Assembly Layer, Owning the Assembly Logic

This tier addresses the strategic crisis at the heart of banking’s current dilemma: who owns the assembly logic between customer intent and transaction execution?

When a customer needs a mortgage, hundreds of micro-decisions occur, including document verification, income confirmation, credit evaluation, property appraisal coordination, insurance procurement, rate pricing, term structuring, and funding source selection. Whoever controls the orchestration of these decisions owns the customer relationship, regardless of who executes individual steps.

Rather than replacing legacy core systems, a multi-year, multi-billion dollar undertaking with existential risk if it fails, the Orchestration Assembly Layer wraps existing infrastructure in an intelligent fabric.

- API Gateway abstracts legacy complexity, presenting modern interfaces to applications while hiding decades of technical debt and inconsistent data models behind unified endpoints.

- Event Mesh creates real-time awareness across all systems, replacing overnight batch processes with sub-second propagation. When a deposit posts, every system knows immediately. Credit models update, fraud thresholds adjust, and customer intent predictions recalibrate.

- Agentic Orchestration deploys AI coordinators that assemble workflows from specialized capabilities, whether those capabilities reside in bank systems or partner platforms. The critical distinction is that the bank controls the orchestrator, while partners provide modules.

- Financial Graph shifts the bank’s view from isolated transactions to complete relationship understanding. Rather than seeing discrete events such as a mortgage payment, credit card purchase, or investment contribution, the graph reveals life stages, intent signals, cascading needs, and intervention opportunities.

The critical insight underlying this tier is that banks can achieve orchestration capability without replacing cores. This dramatically reduces cost, compresses timelines from years to months, and manages risk by maintaining legacy systems as fallback while new capabilities prove themselves.

Tier 3: Systemic Memory Layer, Where Intelligence Compounds

Most banks process billions of transactions annually yet operate with institutional amnesia. Each interaction is processed independently because legacy systems lack architecture for preserving and reusing knowledge across time, across products, and across customer interactions.

The Systemic Memory Layer creates continuous institutional learning:

- Every decision outcome feeds back into models. Did approved loans perform as predicted? Did declined applicants default elsewhere, suggesting the model was too conservative?

- Human expertise becomes scalable institutional knowledge. When underwriters override AI recommendations and those overrides prove correct, the system learns the pattern and incorporates it.

- Architectural intent remains legible. Why was this system designed this way? What assumptions underlie the decision logic? What constraints govern the workflow?

- Regulatory compliance is embedded rather than retrofitted. Every decision generates a complete audit trail automatically, not through manual documentation.

When this layer exists, every transaction strengthens the institution’s collective intelligence. A loan approved today improves credit models tomorrow. A fraud blocked this morning refines detection thresholds this afternoon. A customer interaction this week shapes experience personalization next week.

Without systemic memory, banks never become smarter. They only become busier, processing more volume without accumulating wisdom.

The Assembly-Over-Replacement Philosophy

The most critical aspect of the Sovereign Decision Fabric is what it does not require: wholesale replacement of existing systems.

Traditional digital transformation typically follows a familiar pattern. Consultants conduct extensive current-state analysis, identify legacy technical debt, recommend comprehensive core replacement, and estimate multi-year timelines with multi-billion-dollar budgets. Boards approve based on projected long-term benefits. Implementation begins. Scope expands as hidden complexity emerges. Timelines extend. Budgets overrun. Risk accumulates. Eventually, the program either delivers years late and billions over budget, or it is abandoned entirely with massive write-offs.

The graveyard of failed core banking replacements is extensive and expensive. These failures are not due to incompetence. They involve sophisticated institutions with capable leadership and ample resources. They fail because the architectural challenge is

fundamentally intractable. Replacing systems that embody decades of business logic, regulatory compliance, and operational knowledge while maintaining continuous operations is structurally high-risk.

The Assembly-Over-Replacement approach offers an alternative. Leave legacy cores running, wrap them in intelligent orchestration fabric, and build new capability on top.

A legacy lending core from 1987 continues processing loans exactly as it always has. But now it is exposed through modern APIs, receives data through real-time event streams, and operates under governance from AI models that evaluate every request before it reaches the legacy system. The old core does not know anything changed. It simply processes fewer transactions, as declined requests never reach it, and higher-quality transactions, since only approved, validated, compliant requests arrive.

This pattern applies across banking infrastructure:

- Deposit cores continue managing accounts

- Card processing systems continue authorizing transactions

- Wealth platforms continue tracking portfolios

All operate beneath an orchestration layer that provides intelligence, coordination, and customer experience.

The bank achieves modern capability without the risk, cost, or timeline of replacement. Critically, the bank owns the orchestration layer, the strategic high ground, while legacy systems become implementation details that can be replaced selectively over time if business value justifies it.

Part IV: The Geopolitical Dimension, When Architecture Becomes National Security

The ICBC Proof of Concept: What State Coordination Enables

The Industrial and Commercial Bank of China’s deployment of a sovereign AI model across hundreds of thousands of employees demonstrates what state-coordinated banking architecture can achieve. This is not merely a competitive benchmark. It is a proof of concept for systemic integration that Western banks cannot replicate under current market structures.

ICBC’s advantage stems from four pillars that Western banks structurally lack:

Unified Data Infrastructure

A state mandate for data sharing across financial institutions eliminates competitive hoarding. While Western banks guard customer data as proprietary assets, Chinese banks share data for systemic risk management and collective model training. The result is AI models trained on complete financial system patterns rather than isolated institutional silos.

Patient Capital Allocation

Multi-decade investment horizons without quarterly earnings pressure. While Western banks optimize for near-term EPS and face activist investor pressure, Chinese state-owned banks deploy capital with strategic patience. The infrastructure enabling ICBC’s AI deployment took over a decade to build, an investment difficult to justify to shareholders expecting rapid returns.

Regulatory Pre-Coordination

Compliance frameworks are designed to enable AI deployment rather than constrain it. Regulators and banks co-evolved policy and technology, ensuring requirements supported innovation. By contrast, Western banks navigate fragmented and often conflicting guidance from multiple agencies, each optimizing for its narrow mandate rather than systemic capability.

Sovereign Technology

Stack Complete independence from Western cloud providers, chip manufacturers, and AI model vendors. While initially imposed by sanctions and trade restrictions, this independence became a strategic advantage. There is no geopolitical vulnerability to supply chain disruptions, technology embargoes, or platform policy changes.

The result is not just an impressive technology deployment. It is a systemic architecture that Western banks cannot match without fundamental changes to competitive dynamics, capital market expectations, regulatory coordination, and technology sovereignty.

Chinese State-Coordinated Model vs Western Banks

Illustration 3: Systemic Coordination Advantage - Western banks build AI capabilities in competitive isolation, each solving similar problems redundantly while lacking collective infrastructure. Chinese state coordination provides unified data, patient capital, regulatory alignment, and technology sovereignty that individual Western banks cannot match under current market structures.

The European Response: DORA as Industrial Policy

The European Union’s Digital Operational Resilience Act (DORA) represents the most sophisticated Western regulatory response to this challenge. While framed as operational resilience requirements, DORA functions as industrial policy that forces European banks to build sovereign infrastructure.

By mandating AI stress testing, limiting cloud provider concentration risk, requiring operational independence from third-party technology vendors, and imposing comprehensive incident reporting, DORA compels banks to develop capabilities they might not otherwise prioritize. Banks cannot simply outsource operational resilience to AWS or Azure. They must maintain sovereign alternatives.

The strategic effect extends beyond individual bank resilience. DORA creates market pull for European AI infrastructure providers, establishes regulatory standards likely to be adopted globally through the Brussels Effect, and reduces European financial system dependence on U.S. and Chinese technology platforms.

The U.S. Vacuum: Fragmentation as Strategic Handicap

Meanwhile, the U.S. regulatory approach remains fragmented across multiple agencies, including the SEC, OCC, CFPB, FTC, and FDIC. Each issues guidance from its specific mandate without coordination. The result is that banks navigate conflicting requirements individually, optimize for compliance rather than capability, and achieve neither Chinese coordination advantages nor European sovereign infrastructure mandates.

The competitive outcome is emerging clearly. Chinese banks gain systemic coordination. European banks build regulatory-mandated sovereignty. U.S. banks remain cloud-dependent and fragmented in their approaches.

This is not about individual bank capability. U.S. banks have access to frontier AI technology, sophisticated talent, and ample capital. It is about architectural coordination. Without systemic alignment through data sharing frameworks, regulatory coherence, and technology sovereignty requirements, U.S. banks build capabilities in isolation. Each solves similar problems redundantly while lacking the collective infrastructure advantages their Chinese and European counterparts enjoy.

Part V: The Closing Window and Strategic Choice

Why Timing Is Non-Negotiable

This is not an evergreen strategic consideration that banks can address when convenient. Market structure is forming now, and repositioning becomes exponentially more difficult with time.

The Current Window (2024-2026)

Banks can still choose their path with relative autonomy:

- AI technology is mature enough for production deployment but not yet ubiquitous

- Customer expectations haven't completely ossified around incumbent orchestrators

- Regulatory frameworks are still forming, with opportunity for industry input

- Talent markets remain accessible—AI engineers haven't been completely absorbed by BigTech

- Capital markets remain patient with credible transformation strategies

Approaching Lock-In (2027-2030)

Market structure begins calcifying:

- Orchestration control establishes with early movers who built infrastructure while competitors deliberated

- Customer expectations cement around proven interfaces—switching from familiar platforms feels like downgrade

- Data gravity makes repositioning prohibitively expensive—network effects compound with each interaction

- Regulatory frameworks codify around established architectures—compliance standards reflect incumbent approaches

- Talent and capital flow to demonstrated winners—recruitment and fundraising become difficult for late movers

Post-2030: Permanent Stratification

The industry divides permanently into two categories:

Sovereign Orchestration Platforms: Control customer relationships, own behavioral data, capture platform economics, maintain strategic independence, set industry standards.

Invisible Infrastructure Providers: Provide commodity services (capital, regulatory licenses, settlement), compete on price and efficiency, lack customer relationships, accept utility economics, follow standards set by orchestrators.

The gap between these categories becomes unbridgeable without extraordinary intervention—massive M&A to acquire orchestration platforms, regulatory restructuring forcing open access, or government-coordinated infrastructure building.

Part VI: The Two Paths Forward: A Framework for Decision

Bank leadership faces a binary strategic choice. There is no middle path, no "wait and see," no hybrid approach that preserves optionality. The choice is architectural and existential.

The Strategic Fork

Illustration 4: Banking's Strategic Fork - Two paths with no middle ground. Each path creates self-reinforcing dynamics that become increasingly difficult to reverse over time.

Path A: Accept Infrastructure Status

Some banks will choose, either explicitly through strategic decision or implicitly through inaction, to become invisible infrastructure providers. This path has a logic:

Strategic Rationale:

- Focus on what banks do well: risk management, regulatory compliance, capital allocation

- Avoid expensive, risky transformation programs

- Partner with FinTechs and platforms that have already won customer interfaces

- Compete on operational efficiency and reliability

- Accept utility economics with stable if unspectacular returns

Operational Model:

- Provide Banking-as-a-Service to FinTech orchestrators

- Optimize cost structure for commodity services

- Maintain regulatory licenses and compliance infrastructure as core value

- Compete primarily on price and reliability, not innovation

Financial Outcome:

- Margins compress over time as orchestrators shop for cheapest infrastructure

- Revenue growth limited to industry baseline

- Profitability sufficient but uninspiring

- Valuation multiples remain depressed

- Eventually: consolidation as scale becomes the only remaining competitive advantage

Who Should Choose This Path:

This is a viable path for specific institutional contexts:

- Regional banks serving stable local markets where customer relationships are deeply embedded in community presence, not digital interfaces

- Specialized infrastructure providers (custody banks, settlement specialists) whose value proposition is operational excellence in narrow domains

- Institutions with ownership structures prioritizing stability over growth (mutual organizations, credit unions with member focus)

- Banks lacking capital, talent, or organizational capacity for multi-year transformation

- Leadership teams approaching retirement or transition unwilling to commit to sustained change programs

The Reality of This Choice:

Choosing infrastructure status is not failure, it's strategic clarity about institutional purpose and competitive positioning. But banks selecting this path must accept its implications:

- Strategic independence diminishes over time as orchestrators set terms

- Innovation capacity atrophies as talent migrates to platforms building future capabilities

- Customer relationships become transactional as direct engagement moves to partner platforms

- Regulatory relevance shifts to orchestrators as they become primary customer touchpoint

- Exit options narrow to acquisition by larger infrastructure consolidators or transformation (increasingly expensive as time passes)

The Decision Framework

Boards and executive teams should evaluate this choice through several critical lenses:

1. Institutional Ambition

Does this bank aspire to shape the future of financial services, or participate in a future shaped by others? Neither answer is inherently wrong, but the choice determines the path.

Questions to consider:

- Do we believe our institution should exist independently in 2035, or is eventual acquisition/consolidation acceptable?

- Are we building for the next generation of leadership, or managing for current stakeholders?

- Does our culture embrace transformation, or value stability?

2. Competitive Position

Banks with certain characteristics have stronger foundations for orchestration strategy:

- Strong customer relationships providing engagement data and behavioral insights

- Differentiated brand or market position creating customer preference beyond price

- Geographic or demographic concentration allowing focused orchestration investment

- Specialized capabilities (wealth management, commercial lending, trade finance) difficult for generalists to replicate

Conversely, banks competing primarily on price in commoditized markets (generic retail banking, undifferentiated commercial lending) may lack positioning to succeed with orchestration strategy.

3. Organizational Capacity

Transformation requires capabilities many banks lack:

- Executive leadership: Sustained CEO commitment through multi-year journey with visible setbacks

- Cross-functional coordination: Ability to align technology, risk, operations, business units under unified architectural direction

- Production discipline: Capacity to move from pilots to production at scale, killing failures quickly

- Workforce investment: Willingness to spend 5-10% of workforce costs annually for 3-5 years on retraining

- Technical talent: Ability to recruit and retain AI engineers, orchestration architects, domain specialists

Banks lacking these capabilities face a choice: build them before attempting transformation (adding 12-18 months to timeline), or accept infrastructure status.

4. Capital Structure and Risk Tolerance

Different ownership structures create different transformation capacities:

- Public banks face quarterly earnings pressure requiring Board commitment to protect multi-year transformation budgets despite near-term margin impact.

- Private banks or mutual organizations have structural advantage pursuing patient capital strategies without public market pressure.

- Banks with activist shareholders may find transformation difficult as investors push for short-term optimization over long-term capability building.

Risk tolerance matters because transformation carries real risks:

- Execution risk: Projects may fail, consuming capital without delivering capability

- Organizational risk: Workforce resistance, talent exodus, cultural disruption

- Competitive risk: While bank transforms, competitors may advance (though infrastructure path carries competitive risk of different form)

Choose based on institutional risk appetite and governance capacity to manage transformation complexity.

5. Time Horizon and Urgency

The window for autonomous choice is closing. Banks deciding later face:

- Higher costs as early movers establish patterns others must license or replicate

- Reduced talent availability as AI engineers choose proven platforms over late starters

- Entrenched customer expectations around incumbent orchestrators making displacement harder

- Calcified regulatory frameworks reflecting early mover architectures

Delaying decision is implicit choice of infrastructure path, as difficulty and cost of orchestration strategy increase with each passing quarter.

Part VII: The CodeNinja Sovereign Implementation Framework

For banks choosing Path B, i.e., sovereign orchestration capability, the challenge shifts from strategic decision to operational execution. This is where most transformation initiatives fail: not from lack of vision or commitment, but from inability to move AI capabilities from pilot demonstrations to production deployment at scale.

Why Implementation Expertise Matters

The gap between impressive AI demonstrations and production banking systems handling millions of transactions daily is vast. Most banks discover this through expensive failure:

- Pilots that cannot scale beyond test environments

- Models that fail regulatory review after months of development

- Architectures creating vendor lock-in rather than sovereign capability

- Implementations that fragment rather than integrate institutional intelligence

CodeNinja exists specifically to bridge this gap. We are not generic AI consultants adapting consumer-grade solutions to banking. We are banking orchestration specialists who understand that production deployment in regulated environments requires fundamentally different approaches than technology demonstrations.

Part VIII: Production-Grade Agentic Solutions for Banking Sovereignty

Why Specialized Expertise Matters

The gap between impressive AI demonstrations and production banking systems handling millions of transactions daily is vast. Most banks discover this through expensive failure, i.e., pilots that cannot scale, models that fail regulatory review, architectures that create vendor lock-in, implementations that fragment rather than integrate institutional capability.

CodeNinja exists specifically to bridge this gap. We are not generic AI consultants adapting consumer-grade solutions to banking. We are banking orchestration specialists who understand that production deployment in regulated environments requires fundamentally different approaches than technology demonstrations.

Core Capabilities

1. Banking-Native Agentic Architecture

We design multi-agent systems specifically for financial services orchestration challenges—not general-purpose AI adapted to banking, but agents architected from inception for banking realities:

- Regulatory compliance as architectural constraint, not afterthought: agents that embed ECOA, FCRA, GDPR, AML requirements in their decision logic.

- Explainability native to design: every decision generates complete audit trail automatically, meeting regulatory examination standards.

- Production-grade performance: sub-100ms latency for real-time authorization decisions, handling millions of daily transactions.

- Graceful degradation: systems that maintain service when individual components fail, preserving customer experience under stress.

- Continuous learning in production: models that improve from operational outcomes, not just training data, accumulating institutional wisdom.

2. Sovereign Infrastructure Design

We architect for independence, not vendor dependency:

- Hybrid deployments balancing on-premise sovereignty (for regulated decisions, sensitive data) with cloud leverage (for appropriate workloads).

- Migration pathways from vendor tools to institutional capability, avoiding permanent lock-in.

- Data sovereignty ensuring customer information remains under bank control, meeting emerging regulatory requirements.

- Technology independence using open standards and portable architectures, not proprietary platforms.

- Operational resilience with systems that function if external dependencies become unavailable.

3. Multi-Agent Orchestration Expertise

The future of banking intelligence is coordinated agent swarms where specialized capabilities collaborate. We bring proven patterns:

- Agent coordination protocols: how fraud detection agents interact with credit assessment agents interact with compliance validators.

- Conflict resolution mechanisms: when agents produce contradictory recommendations, systems that synthesize wisdom rather than escalate every conflict.

- Performance optimization: ensuring agent collaboration doesn't create latency bottlenecks that degrade customer experience.

- Explainability across multi-agent chains: audit trails that show how multiple agents reached consensus decisions

- Continuous improvement: as individual agents evolve, orchestration logic adapts maintaining system coherence.

4. Financial Services Domain Knowledge

We understand banking operations, not just technology:

- Fraud pattern evolution: how attacks adapt and how defenses must counter-evolve.

- Credit risk nuance: balancing approval rates (revenue opportunity) against default risk (loss exposure).

- Compliance constraints: how regulatory requirements shape decision logic and limit operational options.

- Customer experience expectations: acceptable latency, required transparency, trust-building interactions.

- Operational realities: shift schedules, exception handling, human oversight models, training requirements.

5. Institutional Knowledge Preservation

Banks' greatest asset is accumulated wisdom about customers, risk, and markets. We ensure this transfers into AI systems:

- Expert interview protocols capturing tacit knowledge from experienced underwriters, fraud investigators, relationship managers.

- Pattern codification transforming institutional practices into agent behaviors.

- Continuous refinement as human experts override agents, systems learn the underlying principles.

- Organizational memory persisting across personnel changes, system upgrades, vendor transitions.

- Cultural alignment ensuring agents behave consistent with bank's values and risk appetite.

6. Rapid Value Delivery

Multi-year transformations lose momentum without early wins. Our methodology delivers measurable business impact in months:

- Phase 1 foundation (6 months): Infrastructure enabling orchestration, baseline metrics established.

- Phase 2 intelligence (12 months): First production agents delivering fraud reduction, approval optimization, processing acceleration.

- Phase 3 orchestration (24 months): Comprehensive workflow orchestration, platform economics emerging.

- Phase 4 sovereignty (36+ months): Sustainable competitive advantage, institutional intelligence as moat.

This matters politically (sustaining executive support through demonstrated progress) and strategically (establishing capability lead while competitors deliberate).

The CodeNinja Difference

Production Discipline from Inception

We don't build pilots hoping they'll scale. We architect for production from day one—ensuring regulatory compliance, data sovereignty, explainability, and operational resilience are embedded, not retrofitted.

Banking Operational Context

We understand how banks actually work—the politics, the processes, the constraints, the culture. This means solutions that succeed in banking reality, not just technical specifications.

Knowledge Transfer Focus

The goal is institutional capability, not perpetual consulting dependency. Our engagement model emphasizes training bank staff, documenting architectural decisions, building internal expertise that persists after external support concludes.

Proven Implementation Patterns

We bring tested approaches from multiple banking deployments—learning from what worked, what failed, what looked good in planning but proved impractical in execution. This accumulated wisdom compresses your learning curve.

Sovereign Architecture Commitment

We architect for your independence. Our recommendations prioritize your long-term strategic control over short-term vendor convenience, even when that makes our engagement more complex.

Conclusion: Architecture as Destiny

Banking's future will not be determined by who has the most advanced AI models, the largest technology budget, the best vendor partnerships, or the most aggressive acquisition strategy. It will be determined by who owns the orchestration layer, the architectural fabric between customer intent and transaction execution where decisions are made, experiences are assembled, and relationships are controlled.

The Sovereign Decision Fabric provides the architectural blueprint for maintaining that control. Through three integrated tiers, Execution Intelligence, Orchestration Assembly, and Systemic Memory, it transforms banks from transaction processors into orchestration platforms where capability compounds rather than fragments, where intelligence accumulates rather than evaporates, where strategic control is preserved rather than outsourced.

The choice is architectural, not technological. Every bank can access similar AI capabilities through vendors and cloud providers. The differentiator is whether those capabilities are deployed within architectures that preserve sovereignty or architectures that create dependency.

The window for autonomous choice is measured in months, not years. Market structure is forming now. Customer expectations are cementing now. Competitive positions are calcifying now. Regulatory frameworks are being established now.

Banks can continue current trajectories, adding AI tools as point solutions, moving faster tactically while losing strategic control, partnering for customer access while accepting architectural subordination, optimizing quarterly results while strategic position erodes.

Or banks can build deliberately, embedding AI as orchestration infrastructure, preserving institutional intelligence within sovereign architectures, establishing themselves as platforms with partners as enhancement modules, accepting near-term investment for long-term independence.

The CodeNinja implementation framework provides the systematic pathway from current state, fragmented pilots, partnership dependency, architectural subordination, to future state, integrated intelligence, orchestration control, strategic sovereignty. This is not theory or aspiration. It is proven methodology delivering production capability that most banks cannot achieve independently.

By the time the dust settles, 2030 and beyond, the industry will have permanently stratified into sovereign orchestration platforms and invisible infrastructure providers. The gap between these categories will be unbridgeable without extraordinary intervention.

In the age of AI-native financial services, those who control orchestration control the industry. Those who hesitate become the infrastructure others orchestrate.

The time for strategic consideration has ended. The time for architectural commitment is now.

Choose sovereignty. Or accept becoming the substrate for the new ecosystem.

There is no middle ground.

Bibliography

- Deloitte. (2024). Banking Survey 2024: AI Adoption in Financial Services. Deloitte Financial Services.

- European Union. (2025). Digital Operational Resilience Act (DORA): Implementation Guidelines. Official Journal of the European Union.

- Federal Bureau of Investigation. (2024). Internet Crime Report 2024. FBI Internet Crime Complaint Center (IC3).

- Federal Trade Commission. (2024). Consumer Sentinel Network Data Book 2024. FTC Bureau of Consumer Protection.

- ICBC (Industrial and Commercial Bank of China). (2024). Annual Report 2024. Retrieved from investor relations and technology implementation disclosures.

- McKinsey & Company. (2024). Global Banking Annual Review 2024. McKinsey Global Institute.

- PwC. (2026). AI Investment Value Survey: Davos 2026 Edition. PwC Strategy& Research.

- World Economic Forum. (2026). Global Cybersecurity Outlook 2026. WEF Centre for Cybersecurity.